What order should I make payments?

Most business books start with the question: "How do I maximise the value of my business?" In reality, most founders start somewhere much more basic:

- "How do I make sure I can pay the mortgage”,

- “keep HMRC happy” and

- “not run out of cash?"

Observing owner-managed businesses, particularly in construction, property and contracting, it is apparent that many business failures are not caused by poor opportunities or lack of ambition. They are caused by a failure to build reserves at the right levels.

The traditional accounting model says:

Sales – Expenses = Profit

The “Profit First model” turns this around:

Sales – Profit = Expenses

This is a powerful behavioural tool because it forces discipline and you can find out more about it in the book https://mikemichalowicz.com/profit-first/ . However, for many UK SMEs, particularly those with volatile cash flows, it needs refinement.

The problem is that there are actually three separate entities that require resilience:

- The business.

- HMRC.

- The owner.

Only when all three are secure should growth become the dominant use of surplus cash. This leads to what I call the Founder Capital Allocation Ladder.

Stage 1: Survival

Every business starts here. The objective is not maximum growth. The objective is survival. At this stage, cash should be allocated in the following order:

1. Business Profit Reserve

A small percentage of every cash receipt is skimmed into a reserve account.

Typically:

- 5–10% of available cash.

This reserve is not a dividend. It is not spending money. It is proof that the business is genuinely creating value and can survive without consuming every pound it receives.

The reserve exists to absorb:

- bad debts

- project losses

- delayed payments

- unexpected opportunities

Most importantly, it changes behaviour. If the business cannot function after removing 5–10% of its cash generation, there is usually a deeper issue with pricing, overheads or working capital management.

2. Tax Reserve

The second allocation is to HMRC.

VAT, PAYE, CIS, Corporation Tax should be treated as already spent.

Too many businesses operate under the illusion that tax liabilities are future problems. In reality, they are present obligations that simply have a future payment date.

The goal should be simple:

- If HMRC demanded payment tomorrow, could the business pay immediately?

If the answer is no, the money is not really available.

3. Owner Survival Reserve

This is the reserve most business literature ignores.

The founder should build a personal liquidity reserve sufficient to cover:

- household costs

- mortgage payments

- family commitments

- unexpected personal expenses

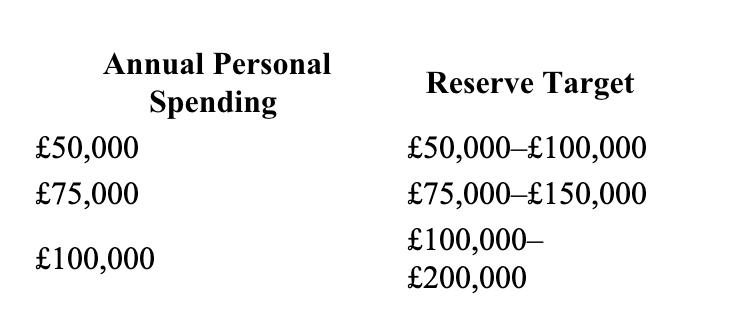

A sensible target is between 12 and 24 months of personal expenditure.

For example:

The impact is profound.

When founders no longer operate from financial anxiety they become more selective, make better decisions and avoid accepting poor-quality work simply to generate cash.

First Inflection Point: Stability

The first major transition occurs when three conditions exist simultaneously:

- Business reserve established

- Taxes fully funded

- Personal reserve established

At this point the business has moved beyond survival.

The founder is no longer asking: "Can we make it through the year?" Instead, they begin asking: "What should we do with surplus capital?" This is the point where many businesses begin to accelerate. Growth becomes a choice rather than a necessity.

Stage 2: Stability

The focus shifts to strengthening the operating platform.

Cash is now allocated between:

- Working capital

- Recruitment

- Systems

- Equipment

- Customer acquisition

- Operational resilience

The business begins creating a buffer between itself and the founder.

Processes become more important than heroics.

Second Inflection Point: Independence

The next major milestone is when the business no longer relies on the founder's daily involvement.

Typical indicators include:

- Management team established.

- Key client relationships shared.

- Systems documented.

- Profitability not dependent on founder effort.

At this stage the founder has effectively created an asset rather than a job.

The key question changes again: "Can the business grow faster than I can personally manage it?" If the answer is no, investment should focus on leadership, systems and structure rather than sales growth. Many businesses become trapped here because founders continue acting as the primary salesperson, estimator, problem solver and decision maker.

Stage 3: Capital Allocation

This is where genuine shareholder value is created. Once reserves are secure and the business operates independently, every surplus pound has competing uses.

Option 1: Reinvest

Invest in opportunities capable of generating returns above the company's cost of capital.

Option 2: Reduce Debt

Debt repayment provides a guaranteed return equal to the interest rate being paid. In higher-rate environments this can become one of the most attractive investments available.

Option 3: Acquire

Use capital to purchase complementary businesses, assets or market share.

Option 4: Distribute

Return capital to shareholders through dividends or share buybacks. At this stage management's primary skill becomes capital allocation rather than operational execution.

Third Inflection Point: Financial Freedom

For many founders this is the least recognised but most significant milestone.

Financial freedom exists when:

- The business no longer requires daily involvement.

- Personal reserves are secure.

- The business generates more income than required for lifestyle needs.

The founder's relationship with risk changes fundamentally.

Growth becomes optional.

This is often when the best strategic decisions are made because they are no longer driven by necessity.

Stage 4: Harvest

Eventually every business enters a harvesting phase.

The triggers may include:

- Founder age.

- Succession concerns.

- Market maturity.

- Lack of attractive growth opportunities.

The objective shifts from:

Maximising enterprise value to Maximising shareholder value extraction.

Cash allocation priorities become:

- Maintain asset quality.

- Preserve resilience.

- Minimise tax leakage.

- Return capital efficiently.

The business becomes a wealth-producing asset rather than a growth vehicle.

Final Inflection Point: Exit

The final transition occurs when ownership itself becomes the focus.

The founder must decide:

- Sell and convert future earnings into immediate capital.

- Transfer and pass ownership to family or management.

- Merge and combine with a larger organisation to create greater value.

- Wind Down and gradually extract value and reduce operations.

At this point, one of the most important questions becomes: "Is the next pound worth more inside the company or in my personal balance sheet?" The answer increasingly shifts toward personal wealth preservation and succession planning.

The Founder Capital Allocation Ladder

As a business matures, the order of priorities evolves.

Survival

- Business reserve

- Tax reserve

- Personal reserve

Stability

- Working capital

- Operational resilience

Growth

- Expansion

- Acquisitions

- Debt optimisation

Wealth Creation

- Shareholder returns

Exit

- Capital extraction

- Succession

- Wealth preservation

The greatest lesson is that growth should not come first. Resilience should, remember:

- A business with reserves can survive mistakes.

- A founder with reserves can make better decisions.

- Only when both are secure does growth become truly valuable.

- The strongest businesses are rarely those that grow the fastest.

- They are the ones that survive long enough to compound.

This framework is particularly relevant to owner-managed construction, property and contracting businesses, where cash flow timing, tax liabilities and founder dependence often matter more than the headline profit figure. The key insight is that the purpose of early profits is not immediate wealth extraction or aggressive growth—it is the creation of resilience. Once resilience exists, growth and shareholder value become far easier to achieve.